Should You Wait Until After the Election to Sell? The Data Might Surprise You

Every election season, a familiar question starts doing the rounds at open homes and in property conversations across New Zealand: Is now really the right time to sell, or should I wait until after the election?

It's an understandable instinct. Elections bring headlines, debate, and a general sense of uncertainty. The story goes that buyers get cold feet, vendors hold back listings, and the market essentially hits pause until the votes are counted and the dust settles.

But here's the thing — when you actually look at the numbers, the picture is far more complicated than that.

What the data actually shows

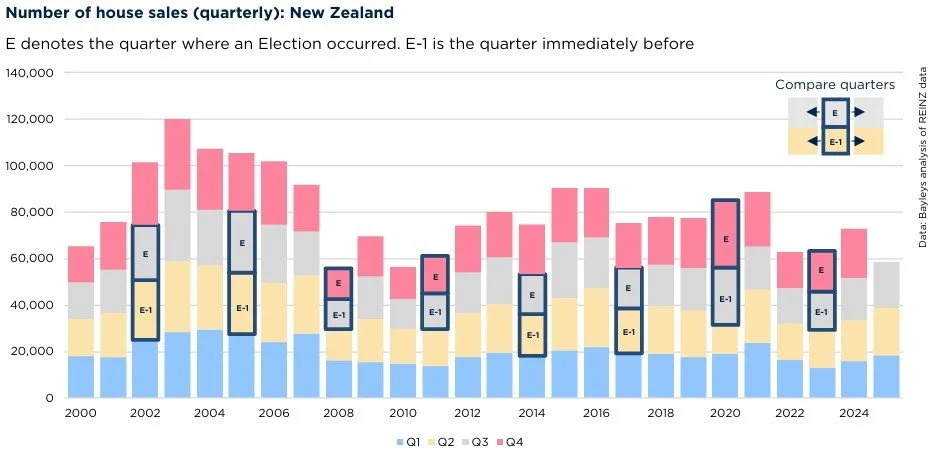

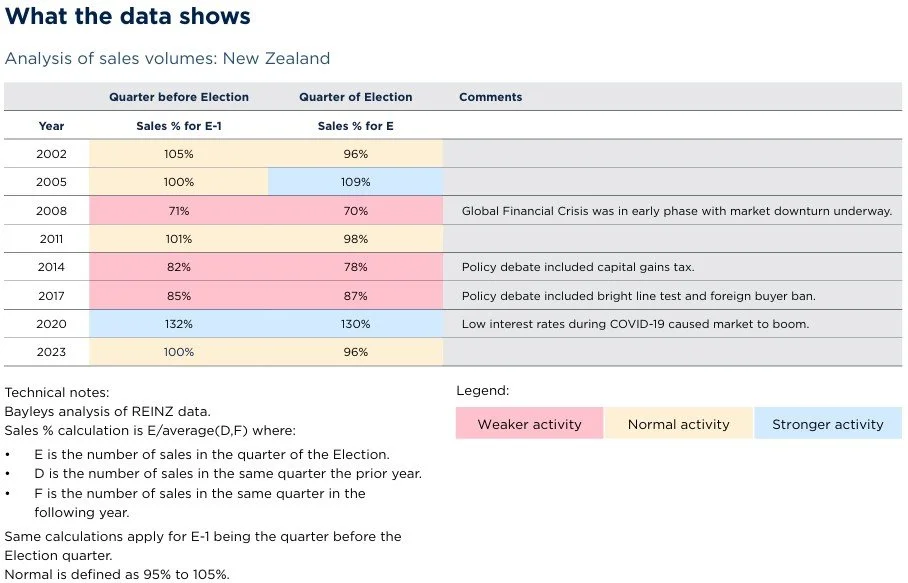

Recent analysis by Bayleys took a close look at multiple election cycles in New Zealand, comparing market activity in the quarters before and during each election year against the periods immediately before and after. The findings? No consistent pattern of an election-driven slowdown.

As Bayleys Senior Analyst Eos Li puts it: "Some indicators rose, some fell, and others remained flat. This makes it difficult to attribute short-term housing market movements directly to election timing alone."

In some election years, activity held firm. In others it dipped — but typically for reasons that had nothing to do with who was running for office.

A walk through the election cycles

Cast your mind back to the early 2000s and there's almost no election effect to speak of. The market was tracking broader economic fundamentals, not the political calendar.

The 2008 election is often cited as a case study in election-driven uncertainty — except it wasn't. That was the Global Financial Crisis. "Market forces overwhelmingly overpowered any election policy effects," Li says. The election happened to fall during one of the worst economic shocks in modern history. Politics wasn't the driver; global finance was.

The 2017 cycle tells a different story too. Activity softened, but by that point the market had already hit its peak. Affordability was stretched, lending was tightening, and momentum was already easing. "This marked a natural turning point. Affordability concerns had intensified, and housing-specific policies began to exert more noticeable influence on market sentiment." Any election-related uncertainty amplified what was already happening — it didn't cause it.

Then came 2020, which flips the narrative entirely. Sales volumes surged during an election year, driven by pandemic-era stimulus and historically low interest rates. Political uncertainty was completely drowned out by macro conditions. And in 2023, the most recent election? Sales remained relatively stable — no notable freeze, no dramatic pullback.

So what actually moves the market?

Across every cycle, one theme emerges clearly: interest rates and credit availability are the real drivers.

Borrowing power, lending accessibility, employment confidence — these fundamentals consistently outperform election-specific policy debate as predictors of market behaviour. Sentiment shifts around elections are real, but they're rarely powerful enough to override economic conditions on their own.

"Unless there are significant macro shocks — a financial crisis, sharp interest rate movements, or major external disruptions — the housing market is likely to continue responding primarily to broader economic conditions," Li says.

Is "election hesitation" even real?

To some extent, yes — but it's more selective and short-lived than the narrative suggests. Certain buyers may pause if major policy changes are on the table (capital gains tax discussions being the obvious example), and some vendors may perceive more caution in the market. But a nationwide freeze? The data doesn't support it.

The idea of an election slowdown persists largely because elections generate intense media coverage, and that amplifies a sense of uncertainty that may not be playing out in actual transaction numbers. "The headlines may focus on politics, but the housing market tends to follow money — and the cost of it."

What does this mean for vendors right now?

With another election on the horizon, the same dynamics apply. Proposed tax changes — including renewed capital gains tax discussions — may shift some investor behaviour. Interest rates may move later in the year. Credit conditions could tighten.

But the core message for vendors is this: timing decisions based on the election calendar alone isn't supported by the long-term data. In fact, holding off to avoid election-period uncertainty might simply swap one form of risk for another — particularly if interest rates or lending conditions shift while you're waiting.

The better questions to ask aren't "Is it an election year?" but rather: What are interest rates doing? What does credit availability look like? What's happening in my specific local market right now?

Because while elections shape headlines, history shows it's the fundamentals that move the market.